CARBON INVENTORY

What it is and why it’s important

What is a Carbon Inventory?

At a highest level, a Nation produces a Carbon Inventory each year as part of its obligations under the United Nations Framework Convention on Climate Change (UNFCCC) and the Kyoto Protocol.

These high-level inventories provide key evidence on greenhouse gas emission trends and inform policy recommendations on climate change. Enabling the monitoring of progress towards our emissions reductions targets.

At a more detailed level, a business may produce an inventory or require a department or project to produce a carbon inventory providing a detail account of its actual emissions or in the case of a planned project, an estimate of the emissions that will be released during both its implementation and later operation.

More detailed level inventories include:

Business inventory

Department inventory

Project carbon inventory providing a detail account of its actual emissions

Planned project may require an estimate of the emissions that will be released during both its implementation and later operation.

Information presented in a carbon inventory can help inform corporate strategies, project portfolios and prioritise actions to reduce emissions and provide benchmarks against which the success of these activities can be measured.

A Carbon Inventory is essentially a quantified list of all items that emit Greenhouse Gas.

The Greenhouse Gas Protocol defines emissions across three scopes i.e. 1-3:

Scope 1 - direct emissions occurring from sources that are owned or controlled by the company.

Scope 2 - emissions from the generation of purchased electricity consumed by the company.

Scope 3 - emissions that are a consequence of the activities of the company but occur from sources not owned or controlled by the company.

The most common used approach in industry today is using ISO 14064 which is an international standard for quantifying and reporting greenhouse gas emissions. The standard guides the development of a GHG inventory that can be compared to other inventories of other organisations regardless of sector or national origin.

ISO 14064-1 defines emissions across six categories rather than the three scopes of the GHG Protocol as described above. View the full Category list.

A process of categorising the carbon emissions within each scope is then undertaken.

In its simplest form a Carbon Inventory for an organisation is a document that records the carbon footprint that a business/project has on the environment.

What is Carbon Inventory Quantification?

Inventory Quantification adopts standard methods for measuring and calculating the GHG emissions attributed to an Organisation. The Intergovernmental Panel on Climate Change (IPCC) provides the world’s most authoritative scientific assessments on climate change and provides guidance for greenhouse gas inventory arrangements and management, data gathering, compilation, and reporting.

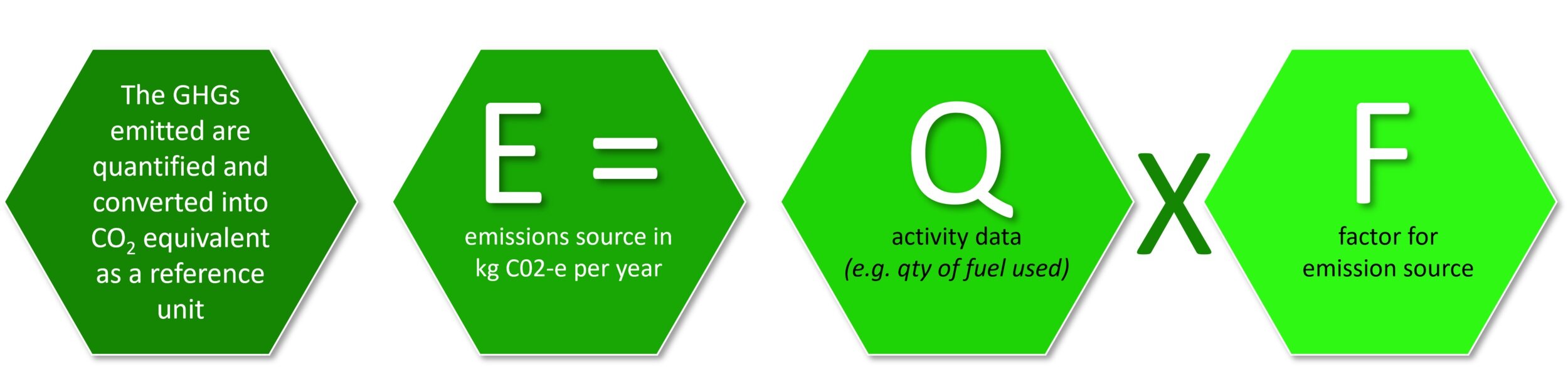

To quantify and report GHG emissions, organisations need data about their activities (for example the quantity and type of fuel used). They can then convert this into information about their emissions (measured in tonnes of CO2-e) using emission factors.

An emission factor allows the estimation of GHG emissions from a unit of available activity data (e.g., litres of fuel used).

The basic calculation used to determine CO2-e is:

CALCULATION METHODOLOGY

This formula applies to the calculation of both CO2-e emissions and individual carbon dioxide, methane and nitrous oxide emissions, with the appropriate emission factors applied for F.

The preferred form of data is in the units that are expressed within emission factor tables, this results in the most accurate emission calculation. If the data cannot be collected in these nominated units, then conversion factors are applied leading to a less accurate quantification.

A basic organisational process map for collecting organisational data for quantification is set out below:

CARBON INVENTORY MANAGEMENT PLAN

The GHG inventory management plan formalises the data collection, procedures and processes the organisation has adopted and which they will be benchmarked against.

This will also form the basis for the accounting principles and future audits.

GHG ACCOUNTING PRINCIPLES

Similar to financial accounting and reporting principles, GHG accounting principles are intended to underpin and guide GHG accounting and reporting to ensure that the reported information represents a true, and fair account of an organisation’s GHG emissions.

GHG accounting and reporting practices are continuing to evolve and are relatively new to most businesses. However, the principles listed below are specified in all international standards, specifically ISO14064-1, and are generally accepted and adopted by a wide range of stakeholders in technical, environmental and accounting disciplines.

For more information of the Greenhouse Gas protocol (or GHG protocol) ‘A Corporate Accounting and Reporting Standard” can be found here.

RELEVANT - Ensure the GHG inventory appropriately reflects the GHG emissions of the company and serves the decision-making needs of users – both internal and external to the company.

COMPLETENESS - Account for and report on all GHG emission sources and activities within the chosen inventory boundary. Disclose and justify any specific exclusions.

CONSISTENCY - Use consistent methodologies to allow for meaningful comparisons of emissions over time. Transparently document any changes to the data, inventory boundary, methods, or any other relevant factors in the time series.

TRANSPARENCY - Address all relevant issues in a factual and coherent manner, based on a clear audit trail. Disclose any relevant assumptions and make appropriate references to the accounting and calculation methodologies and data sources used.

ACCURACY - Ensure that the quantification of GHG emissions is systematically neither over nor under actual emissions, as far as can be judged, and that uncertainties are reduced as far as practicable. Achieve sufficient accuracy to enable users to make decisions with reasonable assurance as to the integrity of the reported information.

Like financial reporting, it’s not done once and forgotten about, rather the approach is to baseline the first year and then adopt a routine of measuring and monitoring the organisational performance. This allows early detection of any change in carbon footprint early on.

References: